– Nepal Economic Forum")

On July 11, 2025, Biswo Nath Poudel, the newly appointed governor of Nepal Rastra Financial institution (NRB), introduced the financial coverage for FY 2025/26 AD (2082/83 BS). A financial coverage is a coverage created and adopted by the central financial institution by way of which it influences people, companies, and the entire financial system. The principle goal of the financial coverage is to keep up value stability within the financial system and maximize combination output and employment degree. Moreover this, the financial coverage additionally works to steadiness worldwide commerce, stabilize monetary markets, and promote capital funding for financial development.

The financial coverage for FY 2025/26 AD (2082/83 BS), particularly, is discretionary and expansionary in nature. Discretionary signifies that the coverage is versatile, with the potential of adapting to the financial scenario. However, expansionary signifies that the central financial institution is aiming enhance financial actions by injecting extra money and lowering rates of interest to extend spending and funding. Thus, this yr’s coverage goals to decrease the price of taking loans for the personal sector and the federal government.

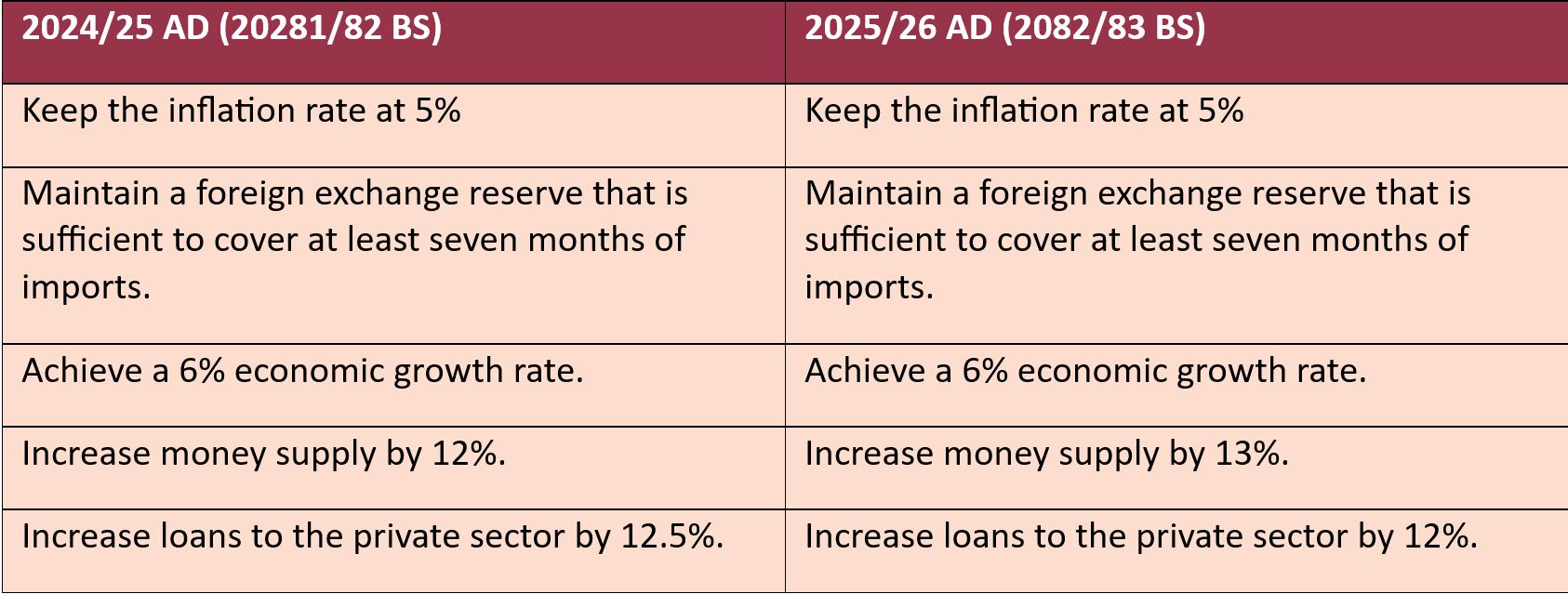

Major Targets of the Financial Coverage

The principle targets of the present financial coverage are much like these set within the final fiscal yr, with a slight change within the development fee of cash provide and loans to the personal sector.

Adjustments within the Curiosity Charge Hall

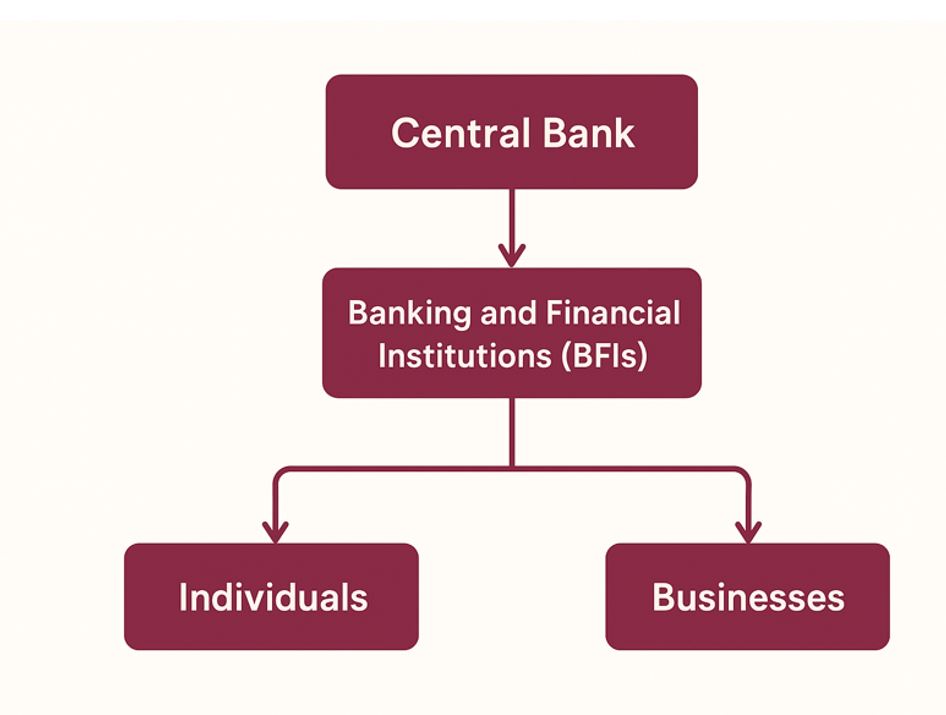

Whereas the targets have remained comparable, there are appreciable adjustments within the rate of interest hall that decide the price of capital held by BFIs. These adjustments, in flip, have an effect on the rate of interest that people and companies obtain on their deposits and should pay for his or her loans from BFIs. The move of financial coverage results is proven in Determine 1.

Determine 1. Move of Financial Coverage Results

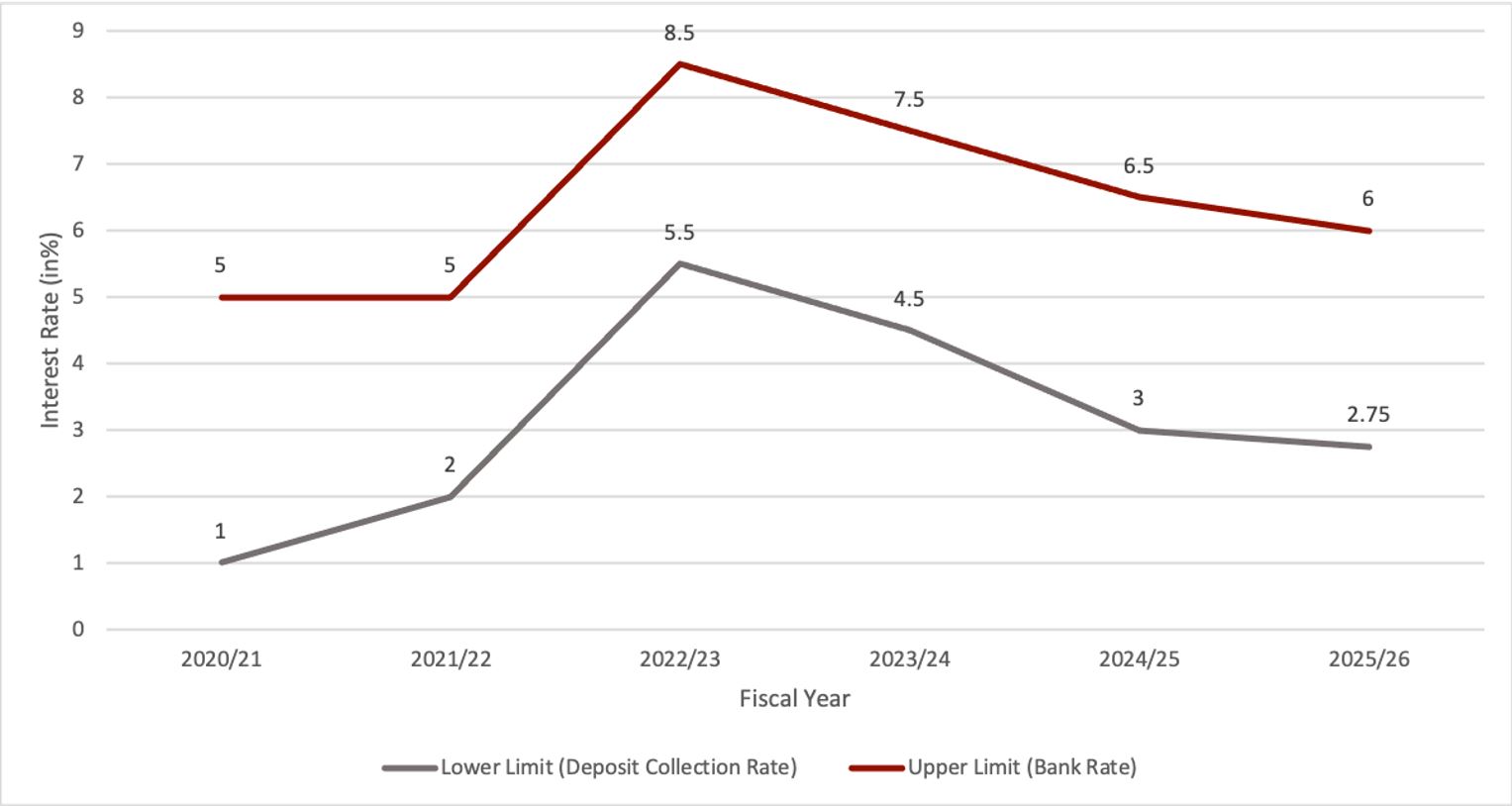

As proven in Determine 2, NRB lowered each the decrease and higher restrict of the rate of interest hall to encourage spending and funding. The decrease restrict decreased from 3% final yr to 2.75%. This fee, also called the deposit assortment fee, is the rate of interest that BFIs can earn on their deposits within the central financial institution. In the meantime the higher restrict decreased from 6.5% final yr to six%. This fee, also called the financial institution fee, is the rate of interest that BFIs must pay on loans taken from the central financial institution. The decrease deposit assortment fee discourages BFIs from depositing on the central financial institution, whereas the decrease financial institution fee encourages BFIs to take extra loans from the central financial institution. This goals to extend the cash provide within the banking sector, which would offer low-cost and easy accessibility to loans for people and companies.

Determine 2. Pattern of the Curiosity Charge Hall From 2021/22 AD to 2025/26 AD

Funding Promotion and International Change Market Adjustments

When it comes to the international alternate market, this yr’s financial coverage consists of numerous guarantees to facilitate and entice international direct funding (FDI). It states that the method of investing in Nepal and taking earnings from these investments might be made easier for international traders. Nonetheless, it doesn’t embody particular provisions to corroborate these statements.

In the meantime, the coverage additionally states that the central financial institution has enough international alternate reserves to cowl imports for 18.2 months. Because of this, the coverage features a provision to permit a Nepali nationwide to alternate as much as USD 3000 per international go to to nations apart from India. It is a USD 500 increment in comparison with final yr.

Laws for Banks and Monetary Establishments

To satisfy the goal of creating it simpler to take loans for people and companies, this yr’s coverage consists of numerous provisions in relation to BFIs. Firstly, the coverage permits finance firms categorised as “C” class, which adjust to worldwide regulatory requirements (Basel I, II, and III), to broaden their deposit assortment and mortgage disbursement actions past earlier limits. Beforehand, these establishments have been restricted to amassing deposits as much as 15 instances their core capital, which is the important monetary reserve appearing as a buffer to make sure stability and canopy potential losses.

Secondly, the coverage consists of borrower-friendly measures to extend entry to credit score. Inside this, the coverage relaxes blacklisting laws associated to cheque dishonor instances, serving to real debtors keep away from harsh penalties. Moreover, BFIs are actually approved to implement lending insurance policies based mostly on prospects’ credit score scores, enabling extra versatile mortgage approvals.

However, the coverage introduced plans to introduce “Neo Banks,” or digital-only banks, to bypass sure phases of conventional banking infrastructure and transition on to digital finance. To assist this transition, NRB can be growing a centralized Know Your Buyer (KYC) system linked to the Nationwide ID, permitting a single replace to be shared throughout all banks. This may simplify entry to credit score and digital wallets, particularly for rural populations missing conventional documentation.

Moreover, to strengthen the monetary market and regulation of BFIs, the financial coverage additionally consists of provisions to determine Home Systemically Necessary Banks (DSIBs) and Systemically Necessary Cost Programs (SIPSs). This forward-looking plan goals to determine necessary monetary establishments.

Insurance policies for the Non-public Sector, Capital Market, and Actual Property

For the fiscal yr 2082/83 BS (2025/26 AD), the financial coverage has launched numerous measures to spice up personal sector exercise and strengthen monetary markets as effectively. To encourage lending, NRB has raised the person restrict from NPR 150 million to NPR 250 million for loans backed by collateral of shares. This enlargement of the mortgage restrict helps traders entry extra funds by way of regulated monetary channels, thereby stimulating capital market exercise. Moreover, the brand new financial coverage permits banks to put money into debentures (bonds) issued by infrastructure-focused establishments, akin to these growing roads, vitality, and industrial parks. These measures collectively goal to spice up capital market exercise, promote funding, assist infrastructure growth, and strengthen market confidence. Nonetheless, these steps require cautious monitoring as additionally they heighten publicity to market volatility.

In the meantime, within the housing sector, NRB has elevated the utmost mortgage restrict for personal residential development or buy from NPR 20 million to NPR 30 million. First-time homebuyers can now borrow as much as 80% of a property’s worth, whereas others can borrow as much as 70%. These adjustments make dwelling loans extra inexpensive, encouraging extra individuals to purchase or construct houses, and thereby enhance the housing and development industries.

Insurance policies for Precedence Sectors

NRB has additionally launched focused lending measures within the new financial coverage to assist restoration, development, and monetary inclusion. To assist communities in earthquake-affected districts like Jajarkot and Rukum, the coverage now permits debtors to reschedule or restructure industrial loans by paying solely 10% of the curiosity due, thereby easing reimbursement burdens.

To spice up tourism and commerce alongside key corridors, companies alongside the Postal or Mid-Hill Freeway and motels or eating places can now entry backed loans as much as NPR 30 million. Nonetheless, to qualify for this profit, motels and eating places will need to have a Division of Meals Know-how and High quality Management (DFTQC) Brand. Such loans might be categorised as designated sector loans and might be offered at an rate of interest premium capped at 2% above the bottom fee, which is decrease than typical.

In agriculture, BFIs can now lend as much as NPR 1 million utilizing self-assessment of debtors’ collateral, which might embody agricultural produce, arable land, or belongings associated to agricultural companies. Moreover, the coverage specifies that in the course of the “grace interval” of those loans, a interval when debtors are given to pay the mortgage with out paying principal and curiosity, banks are required to put aside solely a minimal quantity as a “loan-loss provision.” It is a reserve of cash banks maintain to cowl potential losses if debtors fail to repay. By conserving this provision low in the course of the grace interval, the coverage reduces the monetary burden on banks, encouraging them to supply these loans. Total, this measure goals to assist farmers and small companies by making credit score extra accessible whereas guaranteeing banks can handle dangers successfully.

Furthermore, to assist youths going for international employment, the financial coverage permits banks to offer them with loans as much as NPR 300,000 for males and NPR 500,000 for girls. In response to the brand new coverage, these loans can even be counted as disadvantaged sector loans.

Moreover, by way of the financial coverage, NRB has launched a Regulatory Sandbox to let fintech startups check new merchandise with out rapid regulatory constraints. That is a part of its nationwide “With Debtors: NRB” marketing campaign to strengthen rural outreach and broaden monetary inclusion.

Conclusion

Nepal’s financial system is well-positioned to learn from the present banking system’s excessive liquidity and low rates of interest. Nonetheless, regardless of managed inflation and enough international alternate reserves, lending by banks and monetary establishments has fallen in need of their potential. To deal with this, the NRB has developed the financial coverage to stimulate financial development and promote capital funding from each the personal sector and the federal government. With decrease rates of interest, elevated credit score ceilings, and improved liquidity, the brand new financial coverage creates a extra conducive setting for funding and consumption. These measures present first-time homebuyers with higher monetary flexibility, provide entrepreneurs and farmers enhanced entry to capital, and foster optimism for financial restoration and elevated exercise throughout these sectors.

{kind=link}