Concessional mortgage is a mortgage out there to debtors with extra favorable phrases than out there within the open market. The favorable phrases can embody decrease rates of interest, longer grace and reimbursement durations, or relaxed collateral necessities. The Authorities of Nepal has been offering curiosity subsidies on 10 totally different classes of loans for the final seven years. The curiosity subsidy covers a sure proportion of rate of interest which lowers the price of credit score to debtors. That’s why a concessional mortgage is also known as a “sponsored mortgage” in Nepal. Not too long ago, the federal government considerably restructured the concessional mortgage program. On August 11, 2025, the Council of Ministers accredited the “Curiosity Subsidy for Concessional Loans Procedures 2025” which changed the “Curiosity Subsidy for Concessional Loans Built-in Procedures 2018.” Following this, Nepal Ratra Financial institution (NRB) issued a round, urging Banking and Monetary Establishments (BFIs) to offer concessional loans as per the brand new procedures. The renewed Concessional Mortgage Program will run till July 16, 2030.

Earlier Mortgage Program and Its Influence

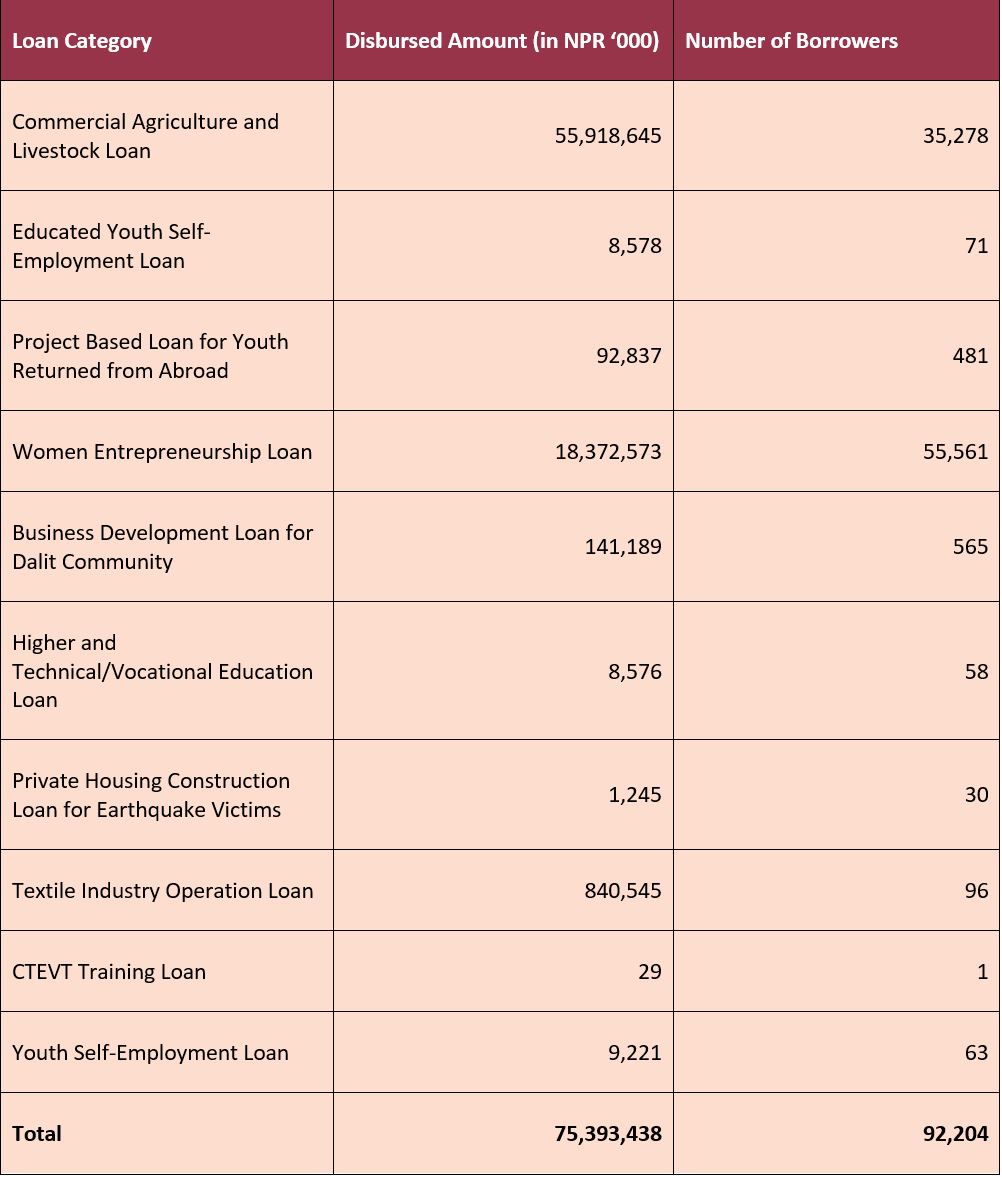

The primary goal of concessional loans is to focus on precedence sectors or teams and provides them monetary help to develop. Previous to restructuring, the concessional mortgage program used to supply loans in 10 totally different classes as proven in Desk 1.

Desk 1. Mortgage Classes with Disbursed Quantity and Variety of Debtors

Supply: Nepal Rastra Financial institution

As of September 17, 2025, NPR 75.40 billion was disbursed to 92,204 debtors underneath these mortgage classes additionally proven in Desk 1. The federal government used to offer 6% curiosity subsidy on Girls Entrepreneurship Mortgage whereas different classes acquired 5% curiosity subsidy. For instance, if a financial institution costs you 10% rate of interest for a mortgage that falls underneath Girls Entrepreneurship Mortgage class, the 6% curiosity subsidy would decrease the efficient rate of interest to simply 4%. It means you must pay solely a 4% rate of interest in your mortgage. To cowl these curiosity subsidies, the federal government spent NPR 28.49 billion. The finance ministry has opened a Subsidy Reimbursement Account at NRB the place the ministry deposits the subsidy quantity. At NRB, BFIs can quarterly apply to reimburse the curiosity subsidy which they’ve offered to the debtors. Nonetheless, the ministry had not reimbursed round NPR 10 Billion curiosity subsidy for the final 2.5 years. Because of this, BFIs didn’t disburse concessional loans struggling loss. Some BFIs had been charging the market rate of interest to debtors, promising debtors to return the sponsored quantity after they obtain the reimbursement from the finance ministry. On September 22, 2025, the finance ministry of the interim authorities launched NPR 9.80 billion to reimburse the pending curiosity subsidy of the final seven quarters. It has given big reduction to BFIs and debtors.

Industrial Agriculture and Livestock Mortgage accounted for 74% of the overall mortgage disbursed whereas Girls Entrepreneurship Mortgage accounted for twenty-four%. The remaining 2% was disbursed in the remainder of eight mortgage classes. Industrial Agriculture and Livestock Mortgage can improve agricultural productiveness. The entry to low cost credit score permits farmers to spend money on improved seeds, prime quality fertilizers and fashionable expertise that enhance their farm manufacturing. Uprety (2022) discovered that the concessional mortgage improved the agricultural productiveness in Dhunibeshi Municipality by round 3872 to 3896 kg per ropani per 12 months. Equally, Girls Entrepreneurship Mortgage can empower not solely girls but in addition the complete financial system. Khanal and Khanal (2024) surveyed 60 girls entrepreneurs in Banke district who borrowed concessional Girls Entrepreneurship Mortgage and located the mortgage elevated their income, created new job alternatives and likewise helped to scale their companies. Regardless that Industrial Agriculture and Livestock Mortgage and Girls Entrepreneurship Mortgage have been efficient, the concessional mortgage program ought to cut back its focus in these two loans and likewise prioritize different classes.

The New Mortgage Program’s Insurance policies

In line with the Workplace of the Auditor Common’s annual report for FY 2023/24 AD (2080/81 BS) , NRB carried out an inner examine on effectiveness of concessional mortgage program by means of a guide. The guide examined 31,664 debtors and located that 7% of the debtors misused the fund, 6% borrowed a number of concessional loans, and 11% had been suspected of misusing the fund. Equally, 25.6% of Industrial Agriculture and Livestock Mortgage debtors had been discovered to misuse the concessional mortgage. As an alternative of utilizing funds for designated actions, debtors had been discovered utilizing the sponsored mortgage to purchase actual property, vehicles, financing overseas jobs, or settling their earlier loans. Some debtors additionally register enterprise within the identify of girls to obtain the ladies entrepreneurship mortgage. The delay in curiosity subsidy reimbursement and misuse of the concessional mortgage program had been the principle foundation to restructure this system.

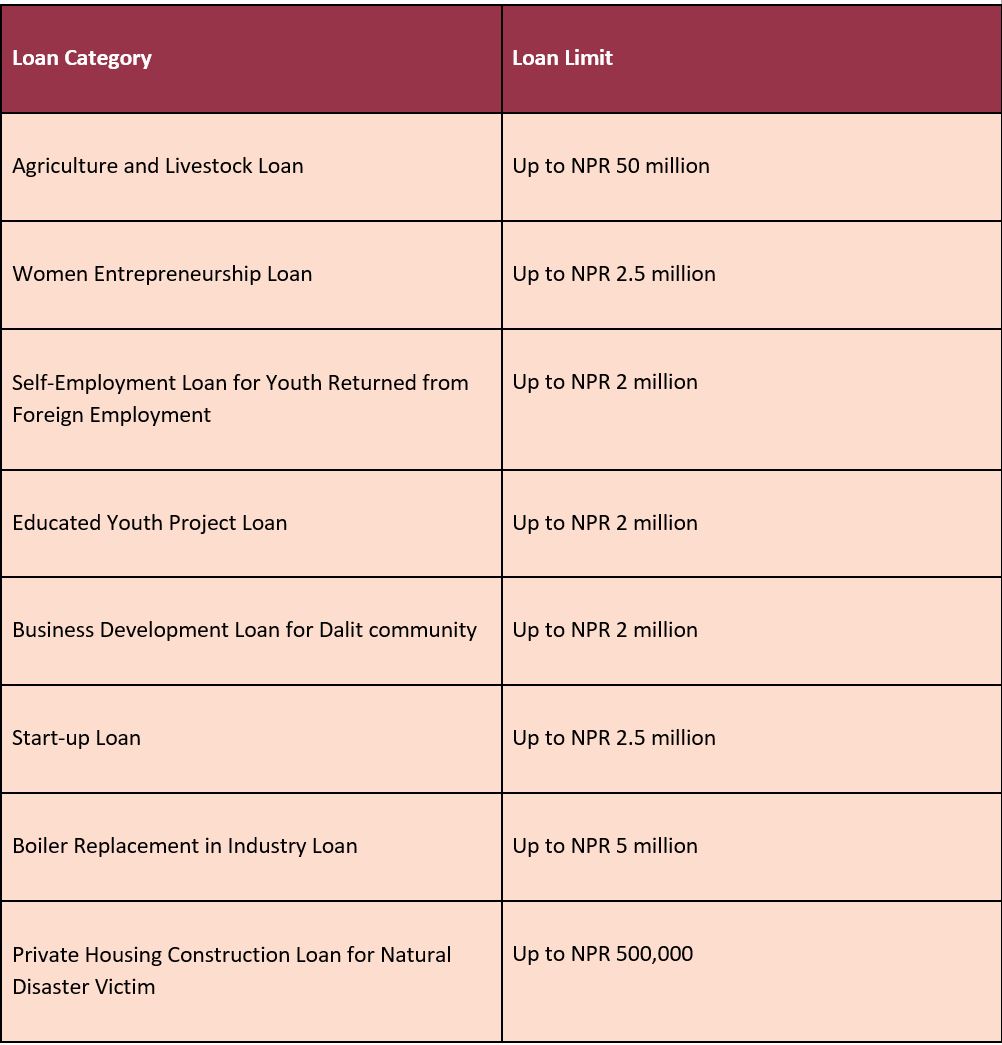

The renewed concessional mortgage program now supplies loans underneath 8 totally different classes. It eradicated the earlier 4 classes and added 2 new classes. Desk 2 exhibits the mortgage classes with most attainable mortgage disbursement quantity.

Desk 2. Classes of Mortgage Below New Concessional Mortgage Program

Apart from Agriculture and Livestock Mortgage, the utmost mortgage restrict of earlier classes has elevated. Nonetheless, the federal government has determined to offer solely a 3% curiosity subsidy on all of the classes. As soon as accredited, debtors can obtain the curiosity subsidy for as much as 5 years.

Challenges of the Present Concessional Mortgage Program

The restructured concessional mortgage program, whereas notable, has a number of challenges which have to be addressed in its early stage. This can assure this system’s attain to focused teams and its total effectiveness. Specifically, There are three main challenges within the present concessional mortgage program:

Consciousness and Entry

Many individuals should not conscious in regards to the availability of a concessional mortgage program and the method to obtain it. Out of 104 samples, Uprety (2022) discovered 25.53% of the respondents had no data on sponsored loans. Such data asymmetry must be addressed to make this system extra inclusive. Uprety (2022) additionally identified that smallholder farmers have poor entry to the sponsored Industrial Agriculture and Livestock Mortgage whereas large-scale farmers are reaping the advantages of this program. Equally, Pradhan et al. (2019) noticed that smallholder farmers would not have clear enterprise plans, face collateral points, and discover the mortgage acquisition course of to be prolonged with intensive paperwork. These hurdles stop them from accessing the sponsored mortgage. As well as, Uprety (2022) discovered that folks from rural areas lack entry to concessional loans in comparison with individuals from city areas. There has not been a lot effort to extend consciousness and entry of this system among the many focused group of individuals.

Requirement of In depth Documentation

In Nepal, BFIs present concessional loans who later reimbursed the curiosity subsidy from NRB. At the moment, Xecuring a concessional mortgage from BFIs is time-consuming and sophisticated, because it entails a variety of paperwork. For instance, BFIs want details about the collateral and its valuation, enterprise plans, insurance coverage, financial institution statements, tax clearance, and plenty of extra paperwork to course of the mortgage. That is cheap from the BFIS’ viewpoint as they wish to reduce the chance by stopping mortgage defaults. Nonetheless, the intensive documentation requirement has turn out to be a hurdle for potential debtors which discourages them from making use of for the mortgage. Uprety (2022) discovered that 74% of the concessional mortgage debtors from their pattern declare the mortgage process to be prolonged, involving intensive paperwork. Amongst 104 samples, he additionally discovered that 68.57% have by no means utilized for sponsored loans, considering it’s a problem to obtain the mortgage. Subsequently, BFIs have to ease the mortgage course of with minimal documentation necessities.

Ample Monitoring and Supervision

Monitoring and Supervision is likely one of the key challenges of the concessional mortgage program. It determines whether or not the funds are used for designated actions or not. Below the brand new process, there are stricter rules for monitoring and supervision of this system. In line with the “Curiosity Subsidy for Concessional Loans Procedures 2025,” BFIs are required to observe the effectiveness of concessional mortgage applications. They should submit details about the quantity of concessional mortgage disbursement to NRB on a month-to-month foundation. Beforehand, they needed to submit this on a quarterly foundation. In addition they want to examine the utilization of loans a minimum of twice a 12 months and submit the report back to NRB. It was once optionally available earlier than. However, NRB is answerable for each the onsite and offsite monitoring and supervising the concessional mortgage program to forestall its misuse. It additionally publishes the names of debtors who’ve borrowed greater than NPR 10 million as a concessional mortgage on its web site. For efficient monitoring and supervision, each NRB and BFIs must be accountable.

Conclusion

There are substantial adjustments within the new concessional mortgage program. It lowered the variety of mortgage classes and sponsored rate of interest whereas growing the mortgage restrict. We discovered elevating consciousness on concessional mortgage program among the many focused group of individuals, simplification of the documentation necessities, and efficient monitoring and supervision can lead to profitable execution of this system and forestall the misuse of the fund. The concessional mortgage program can improve home manufacturing, generate new employment alternatives, and promote entrepreneurship if applied successfully.

Pawan Raj Dallakoti holds a BA in Liberal Arts with a focus in Japanese Enterprise and the International Economic system from Doshisha College, Japan. He additionally studied for a 12 months on the College of Political Science and Economics, Waseda College as an alternate pupil. He’s at present a Analysis Fellow on the Nepal Financial Discussion board (NEF). Previous to becoming a member of NEF, he interned on the Nationwide Coverage Discussion board (NPF) and the SAARC Secretariat. His analysis pursuits lie in evidence-based policymaking in agriculture, vitality, and setting.

{kind=link}