FUTURE READY

Compiled by Yamini Sequeira

POWERING A CASHLESS ECONOMY

Avanthi Colombage opinions the state of play and way forward for digital funds

What stands out to her is the nation’s resilience and its continued openness to adopting improvements that may meaningfully improve lives, whereas elevating the financial and digital panorama.

“Over the previous couple of years, we have now seen tangible progress in client consciousness, a modernising banking ecosystem, increasing service provider acceptance and powerful regulatory assist. Contactless funds and cell pushed options are gaining widespread traction, reinforcing confidence within the route of journey,” she provides.

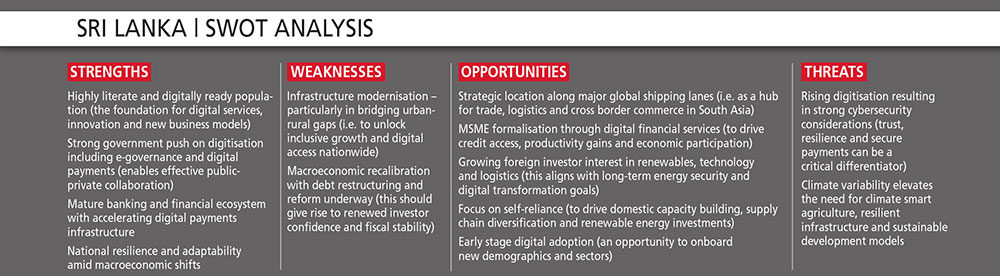

Geared up with a formidable literacy charge of 97.4 % (which is a file excessive), the nation is uniquely positioned to speed up digital funds adoption and unlock the complete potential of a digitally enabled financial system.

INCLUSIVE GROWTH Colombage notes that “a essential alternative throughout rising markets is bringing micro, small and medium enterprises (MSMEs) into the formal digital financial system, significantly in excessive influence industries similar to tourism. In Sri Lanka, that is already underway by sturdy public-private collaboration.”

“Essentially the most noticed vulnerabilities – similar to uneven digital adoption throughout segments, gaps in city and rural infrastructure, evolving cybersecurity capabilities and the necessity for continued client training as digital utilization scales – are being addressed as shared alternatives,” she assures.

As fee ecosystems scale, cybersecurity and fraud prevention naturally change into areas of focus.

She observes that “presently, the nation is progressing in step with world greatest practices, together with the adoption of tokenisation to cut back publicity of delicate information and strengthen client belief.”

“Moreover, Sri Lanka demonstrates how rising market vulnerabilities will be remodeled into catalysts for development when addressed early by collaboration,” Colombage explains.

DIGITAL ECONOMY Commenting on probably the most essential reform wanted to speed up money to digital migration, she states that “Sri Lanka should speed up the digitisation of all authorities funds – each collections and disbursements – on open, interoperable and low price infrastructure, in order that the state itself turns into the first driver of money to digital adoption throughout the financial system.”

By guaranteeing that each citizen and micro enterprise can obtain, retailer and use cash digitally by authorities touchpoints, this reform advances monetary inclusion.

This can deliver casual and underserved populations into the formal monetary system, whereas enabling entry to financial savings, credit score and digital financial participation.

Interoperability is essential to make sure that digital funds are handy, accessible and scalable. When programs work collectively – permitting a client to pay any service provider on any platform, utilizing any pockets or card – all the ecosystem advantages.

Colombage explains: “If the ecosystem is fragmented, shoppers face friction, confusion and inconsistency. Retailers could have to take care of a number of programs, rising working burdens. Prices rise throughout the ecosystem because of duplicated infrastructure. Belief erodes when digital funds don’t work in every single place and innovation slows as a result of options should be rebuilt for separate networks as an alternative of 1 unified atmosphere.”

Over time, fragmentation creates a two velocity financial system: one phase advantages from digital comfort whereas one other stays excluded.

“In a rustic the place casual staff, SMEs, and micro entrepreneurs type the spine of the financial system, true inclusion means enabling people and companies to take part totally, confidently and productively within the digital monetary system,” she emphasises.

And she or he provides: “This requires easy, safe and reasonably priced instruments that deliver on a regular basis commerce into the formal ecosystem.”

Digital funds alone can not drive inclusion; they need to work hand in hand with digital id, entry to credit score and powerful monetary literacy to construct sturdy rails to the final mile. In her view, these three components allow customers to confidently undertake digital instruments, construct monetary histories safely and unlock financial alternative.

Accordingly, digital funds should be complemented by initiatives to enhance digital literacy, increase credit score entry and set up safe digital id programs. Designing an ecosystem that uplifts rural communities is the following main trade leap – and a strong pathway to enhancing livelihoods.

The important thing shall be to offer options which are easy and reasonably priced, in order that anybody, anyplace can take part while not having costly gadgets or advanced onboarding processes.

Over the following decade, playing cards, cell wallets and account to account funds will coexist in way more seamless and interconnected methods than we see immediately. Playing cards will proceed to play a foundational function, evolving past bodily plastic into safe digital credentials powering all types of fee.

SECURE PAYMENTS On the coronary heart of this evolution is tokenisation, which replaces delicate card particulars with a novel digital token, lowering the danger of fraud whereas enabling safe funds throughout playing cards, wallets, wearables and on-line channels.

Cell wallets will proceed to increase because the on a regular basis interface for digital life, significantly amongst youthful, cell first shoppers.

As Colombage factors out, “in Sri Lanka, this shift is already seen. The nation is now at 64 % contactless penetration, greater than doubling in solely two years, with faucet to pay changing into a lifestyle throughout shoppers, retailers and companies.”

“Account to account funds will even develop, significantly for presidency transactions, invoice funds and recurring use circumstances. Nonetheless, they’re only when mixed with sturdy safety, fraud safety and dispute administration to make sure belief as volumes scale,” she provides.

In Sri Lanka, this multi rail future is already taking form…

“Tokenisation will make digital funds far safer throughout playing cards and cell wallets whereas biometrics will simplify authentication for thousands and thousands of customers,” she asserts.

AI will change into pervasive throughout the funds ecosystem, working together with tokenisation and biometrics to repeatedly improve fraud detection, threat intelligence, safety and more and more personalised fee experiences.

Invisible, embedded and frictionless are – and can stay – the guiding rules for funds.

“From mobility apps and e-commerce to subscriptions, shoppers count on velocity, safety and ease while not having to consider the underlying fee technique. But, larger invisibility should include stronger safeguards,” Colombage explains.

She continues: “This implies modernised regulation, clear information safety requirements and stringent client rights, all supported by the newest applied sciences.”

“The velocity, scale and interconnectedness of the world have modified. Funds have developed extra within the final 5 years than within the earlier 50. The acceleration of digital commerce, contactless funds, cell wallets and real-time experiences has basically reshaped how individuals and companies transfer cash,” she muses.

Even in a extra advanced world, the function of digital funds is evident: they assist financial resilience, unlock new alternatives for companies and shoppers, and assist international locations combine extra seamlessly into the worldwide financial system.

{kind=link}