This text is from the fifth version (April–June 2026) of 38 North’s quarterly product, North Korea Briefing, that displays key inside developments in North Korea. For the total sequence, click on right here.

Two developments outlined the North Korean economic system within the first half of 2026. The primary was financial: the gained fell steeply and market costs surged alongside it. The second was a windfall in mineral exports, pushed by international, notably Chinese language, demand for tungsten fairly than Pyongyang’s personal doing. Collectively they reveal a single situation: North Korea can nonetheless earn significant overseas alternate when international costs transfer in its favor, even because it loses its grip by itself forex at residence. The windfall rested on a unstable worth the state neither set nor managed, whereas the forex instability was largely homegrown—that means the exterior positive factors did little to stabilize the economic system, and the 2 developments are finest understood as largely impartial.

A Sliding Received and Financial Inflation

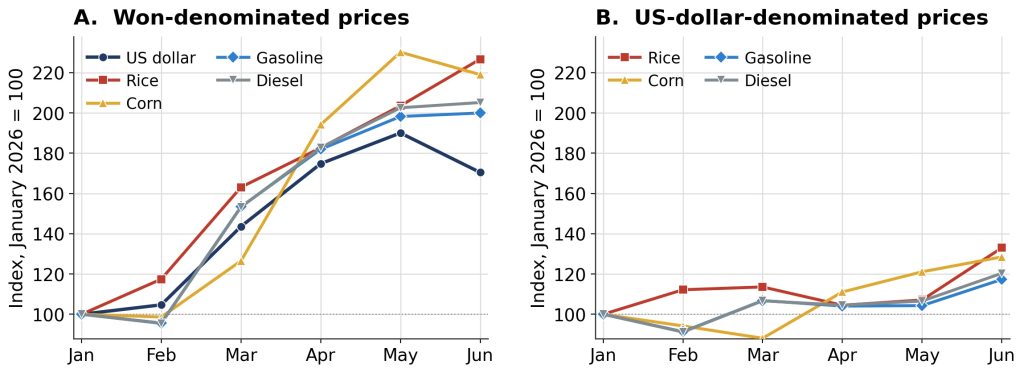

The clearest sign of the primary half got here from the gained, whose market alternate charge fell steeply in opposition to the US greenback and the Chinese language yuan as costs in gained phrases rose: the greenback climbed to a Might peak about 90 % above its January stage—from roughly 37,250 to 70,800 gained—earlier than easing in June, whereas gained costs for rice, corn, gasoline, and diesel roughly doubled (Desk 1).[1] The acute depreciation ran from March to Might, with the gained partly retracing in June. Even granting that non-public markets might have receded because the pandemic period recentralization, making retail costs a narrower gauge, the transfer learn as an economy-wide financial occasion, not a market-specific one. It runs by the alternate charge on which the nation’s closely dollarized transactions are primarily based. Over an extended horizon, the size is appreciable: the greenback’s gained worth has risen roughly seven-and-a-half-fold since early 2024, with the gained shedding most of its exterior worth in only two years.

The decisive proof that depreciation, not shortage, drove the surge comes from repricing these items in laborious forex. By way of June, greenback costs rose solely modestly—rice from $0.41 to $0.55 per kilogram, gasoline from $1.03 to $1.27, and corn from $0.10 to $0.13—at the same time as gained costs doubled (Determine 1, Panel B); gasoline, which has no spring lean season impact, moved in near-lockstep with grain. Costs rose as a result of every gained purchased steadily much less overseas alternate; within the North’s dollarized markets they’re set successfully in opposition to the greenback.

The distributional consequence follows instantly. With greenback costs broadly secure, those that earn or maintain laborious forex—merchants and the donju entrepreneurial class—noticed their actual buying energy largely preserved by June. The burden fell on the won-dependent: state enterprise wage earners and others paid in gained, whose nominal incomes don’t regulate with the alternate charge. For them, a doubling of meals and gasoline costs in gained inside months is a pointy, regressive real-income shock that any combination inflation determine would understate. These strains are seen in market habits, with an accelerating flight from the gained and a coercive state response.[2]

Context and Implications

Why the gained is falling is tougher to determine. A transfer this huge—a near-doubling in months—is much bigger than any believable commerce stability swing may produce, and there’s no signal overseas alternate earnings had been contracting. If something, abroad labor and mineral receipts had been rising, with labor earnings specifically bolstered by the continued dispatch of staff to Russia amid the struggle in Ukraine.[3] That factors away from a overseas alternate scarcity towards home causes, of which two match the proof and usually are not mutually unique.

The primary is financial. Extra gained liquidity, past what laborious forex provide can again, would depreciate the gained pretty mechanically. Two channels plausibly drove it: financing the regime’s development and regional growth commitments, and the marketing campaign of state wage and worth will increase North Korea has pursued since late 2023 to revive its deliberate economic system and state commerce. A cupboard decision lifted nominal public sector wages roughly tenfold—reportedly as much as 40 or 50 instances in precedence sectors—alongside parallel hikes in state-set costs.[4] Paying out much more nominal gained with out matching output is financial growth. Observers tie this on to rising costs, and broad, roughly proportional co-movement of costs and the alternate charge is its signature. On this studying, the marketing campaign is itself a deliberate repricing of the state sector, and the gained’s slide could also be a tolerated—even meant—consequence fairly than an undesirable aspect impact; the information can not settle intent, because the proof matches an undesired byproduct of financial financing equally effectively.

The second trigger is expectational. A lack of confidence within the gained, doubtlessly self-reinforcing as soon as depreciation begins, can drive households and merchants out of gained and into {dollars} and yuan regardless of fundamentals. The general public’s mistrust has deep roots, going again to the 2009 forex redenomination, and mass wage will increase financed by cash creation, together with the state’s crackdowns and warnings in response to the gained’s steep fall, have solely pushed additional flight from the native forex.[5]

A Tungsten Windfall: Value, Not Effort

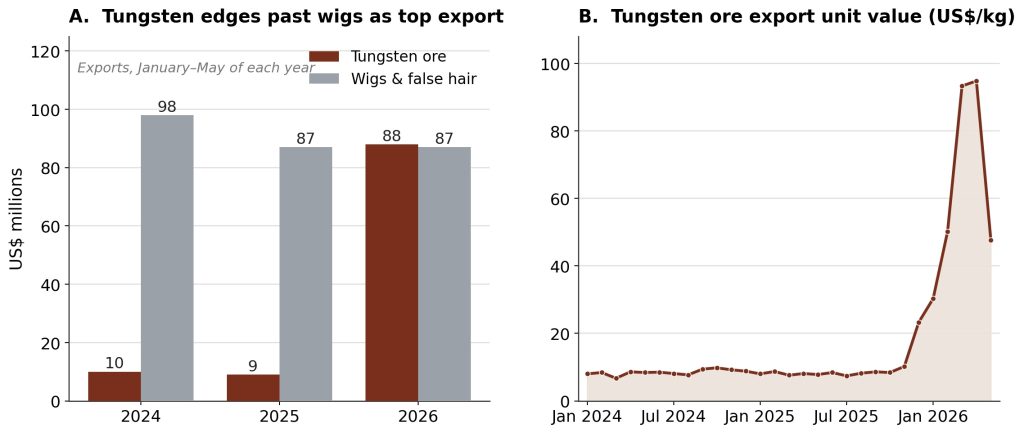

The primary half’s different notable growth was exterior and largely unrelated to the gained’s slide: a surge in mineral export earnings. Exports to China rose 68 % year-on-year over January-Might, to $287 million, with roughly two-thirds of that enhance from a single export line: tungsten ore, whose worth leapt almost tenfold, from about $9 million a yr earlier to $88 million (Desk 2).

The windfall was nearly purely a worth phenomenon. Cargo tonnage rose solely about 15 %; the typical unit worth jumped from round $8 to almost $70 per kilogram—some 98 % of the earnings development (Determine 2). The unit worth proved unstable: the month-to-month unit worth spiked above $90 per kilogram in March and April earlier than halving to round $48 in Might. The trigger lies solely outdoors North Korea: China, which controls greater than three-quarters of world tungsten provide, positioned tungsten merchandise beneath export licensing in February 2025 and tightened controls by 2026; benchmark costs for ammonium paratungstate rose about 218 % over 2025 and reached file highs in early 2026.[6] As a marginal provider to Chinese language processors, North Korea obtained much more for roughly the identical quantity.

Context and Implications

The shift has reshaped the nation’s export profile. Mineral ores, barely a tenth of gross sales to China a yr earlier, now make up a few third. For years the North’s largest export had been wigs and false hair—the labor-intensive output of its processing-on-commission commerce—however over January-Might 2026 tungsten drew stage and narrowly edged forward for the primary time. The change marks a transfer from an export reflecting North Korean labor to at least one reflecting a worth the nation neither units nor controls. The earnings are actual, however they symbolize a windfall hostage to a unstable international market, because the Might worth pullback illustrates, fairly than proof of sturdy productive capability.

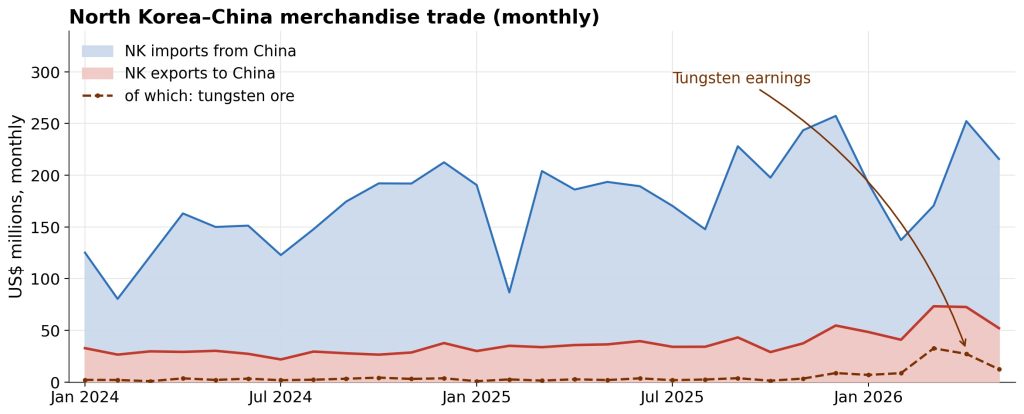

Substantial because it was, the windfall does little to change North Korea’s exterior accounts (Determine 3). At roughly $16 million a month in additional earnings, it’s dwarfed by a $194 million month-to-month import invoice; the merchandise deficit with China was basically flat year-on-year. The half-year’s two tales are thus impartial: the tungsten increase was far too small to maneuver the overseas alternate market, so it neither brought on the gained’s slide nor cushioned it.

Outlook

Each tales carry ahead on separate tracks. President Xi Jinping’s June 8-9 state go to to Pyongyang—his first since 2019 and his first abroad journey of 2026—signaled a deliberate warming as Beijing strikes to reassert its affect amid deepening North Korea-Russia ties and prospects for eventual US-North Korea talks. To the extent the go to results in expanded commerce, power, or different help, it is among the few forces that would meaningfully broaden the North’s overseas alternate inflows and ease stress on the gained—although any such impact is a narrative for the second half, and previous Chinese language help has not often been transformative.

June’s partial rebound within the gained is welcome however too short-lived to be relied upon; its path will hinge much less on the autumn harvest than on how a lot liquidity the authorities proceed to inject to finance precedence initiatives. The tungsten windfall will rise and fall with a market set in Beijing and past—profitable whereas it lasts, however no basis for a restoration.

{kind=link}